Since 2016, the hospital sub-sector in Benin, like the wider health system, has undergone profound reforms that have led to the establishment of new or reorganised structures, such as the National Council of Hospital Medicine (CNMH), responsible for strategic guidance, and the Directorate-General of Hospital Medicine and Diagnostic Investigations (DGMHED), in charge of operational coordination.1,2 These transformations have been accompanied by legislative and regulatory reforms aimed at revitalising hospital governance and improving service delivery.

Key legal instruments include the law on public enterprises in Benin3 and its implementing decrees, as well as decrees on hospital governance that establish public hospitals as public institutions of a social and scientific nature, granting them financial and managerial autonomy based on private-sector accounting principles. This institutional shift marks the transition from an “administrative hospital” model to an “enterprise hospital” model4,5 and explicitly aims to improve hospital performance.6 It requires hospitals to mobilise greater levels of own-source revenue to finance their operations and investments.

At this early stage of implementation of the new paradigm, the financial resources of public hospitals in Benin are derived both from government subsidies and from internally generated activities, such as pharmaceutical sales, consultations, medical procedures and diagnostic investigations.7 While the performance of the hospital-enterprise model has been widely studied in Europe and North Africa,8–10 the evidence base remains limited in sub-Saharan Africa, particularly in Benin11 limits the assessment of the relevance of these reforms. Key questions therefore remain: what is the contribution of this model to hospital economic performance? Does this reform improve the hospital’s efficiency of financial resource mobilisation?

Within the current context of reforms in Benin, this study, whose objective was to assess the effectiveness of the financial resource mobilisation system of a teaching hospital and its economic performance, helps to address this gap in empirical evidence and provides insight into the financial management of public hospitals.

Based on a conceptual framework inspired by Donabedian,12 the study examined the structures and processes of resource mobilisation, the outcomes achieved, and contextual factors influencing the performance of the hospital’s financial management unit.

METHODS

Study setting

The study was conducted at the Centre Hospitalier Universitaire de la Mère et de l’Enfant-Lagune (CHUMEL), the main public referral hospital dedicated to maternal and child health in Benin. A pioneer in quality improvement, CHUMEL obtained its first ISO certification in 2005, which was renewed and expanded in 2017 to ISO 9001:2015, now covering several key processes, including pharmacy services, vaccination and social services.

The hospital is equipped with a comprehensive technical platform and employs 690 staff members, of whom 39.1% are civil servants and 7.7% are physicians. With a bed capacity of 304 beds, hospital activity is substantial, with 6,364 deliveries recorded in 2022, 52.8% of which were caesarean sections, and more than 30,000 outpatient consultations across maternal and child health units.

From an organisational perspective, CHUMEL operates under Decrees No. 2020-498 of 7 October 2020 and No. 2022-121 of 23 February 2022, which define the operational rules of public hospitals and the legal status of teaching hospitals. The institution comprises approximately twenty medical and medico-technical departments structured around maternal and child health poles.

Study methods

Study design and period

This was a descriptive, evaluative cross-sectional study covering the period from January 2021 to June 2023. Data collection was conducted between October and November 2023.

Study population and eligibility criteria

The source population included staff members, service users and administrative documents from CHUMEL. The target population consisted of:

-

key informants from the general management involved in revenue collection;

-

operational staff such as accountants, cashiers and support personnel (“green-collar” workers);

-

medical and nursing staff;

-

service users and their accompanying persons;

-

accounting and financial documents covering fiscal years 2021, 2022 and the first half of 2023.

Inclusion criteria were based on length of service (≥ six months), presence during data collection and provision of free and informed consent. Staff under disciplinary or legal sanction and respondents with unusable data were excluded.

Sampling

A mixed sampling approach was adopted, including:

-

exhaustive sampling for senior managers, revenue collection staff, support personnel and documentary sources;

-

probabilistic sampling using systematic random selection for service users and accompanying persons.

The minimum sample size for service users, estimated at 250 respondents, was calculated using Schwartz’s formula, assuming an expected annual mobilisation rate of 0.8, a 5% alpha risk and 5% precision.

Data collection techniques, tools and process

Three complementary approaches were used:

-

Document review: extraction of data from accounting records, activity reports and financial databases using standardised data extraction forms.

-

Semi-structured interviews and direct observation: conducted with managers, revenue collection staff, medical and support personnel using interview guides and observation checklists.

-

User-administered questionnaires: designed to capture socio-demographic characteristics, perceptions and experiences related to payment for care.

Data collection was carried out by a team of two trained investigators under the supervision of a field supervisor. A pre-test was conducted in another teaching hospital in Cotonou to validate the data collection tools.

Service users were surveyed either within the hospital or outside the facility, depending on their convenience, while managers and actors involved in financial management were interviewed at their respective workplaces in accordance with the predefined selection criteria. The selection of surveyed users was conducted using a sampling frame constructed from medical records and registers. Financial data were collected from management tools made available by the hospital administration and revenue collection units.

Variables and operational definitions

The primary variable was the overall annual financial resource mobilisation rate (N), defined as the average of internal (R) and external (S) collection rates.

The annual collection rate was defined as the ratio between revenue actually collected over one year and total expected revenue over the same period:

N=Rie+SeRia+Sa

where R denotes revenue, i internal, e collected, S subsidy and a expected.

Collection performance was categorised as good (N ≥ 0.9), moderate (0.7 ≤ N < 0.9) or poor (N < 0.7). This threshold of 0.9 is adopted empirically to safeguard financial viability, as it entails more stringent financial governance requirements than the 0.8 benchmark commonly used in health sector reports in Benin, and is closer to the 0.95 threshold frequently applied in high-income countries operating under the hospital enterprise model.

Secondary variables related to:

-

structure: human resources, equipment, infrastructure and management tools;

-

processes: organisation of revenue collection, control mechanisms, professional practices and traceability;

-

outcomes: internal and external collection rates, revenue leakage and unpaid bills;

-

environment: users’ socio-economic profiles and perceptions.

Data processing and analysis

Qualitative data derived from interviews were analysed to identify key parameters and to compute indicators used to characterise the financial resource mobilisation process. The analysis, which was primarily descriptive, focused on practices and outcomes within the facility.

Quantitative data were entered, cleaned, and analysed using Excel 2013. They were summarised using means ± standard deviations or medians with interquartile ranges, depending on their distribution. Frequencies were also calculated. Summary tables and figures were produced to compare indicators across financial years and stakeholder groups.

Ethical considerations

Formal authorisation was obtained from IRSP, the Ministry of Health and the General Directorate of CHUMEL. All participants were informed about the study objectives and provided informed consent. Confidentiality, anonymity and adherence to professional ethical standards were ensured. Only aggregated data were used for publication.

RESULTS

This study assessed the revenue collection system at CHUMEL in 2023 based on interviews with eight (8) key informants, sixty-one (61) operational actors and two hundred and fifty-one (251) service users. Results are presented according to the Structure–Process–Outcome analytical framework, supplemented by an analysis of the environmental context.

Structural component of the revenue collection system

The structural assessment focused on human resources, infrastructure, equipment and the regulatory framework.

Human resources

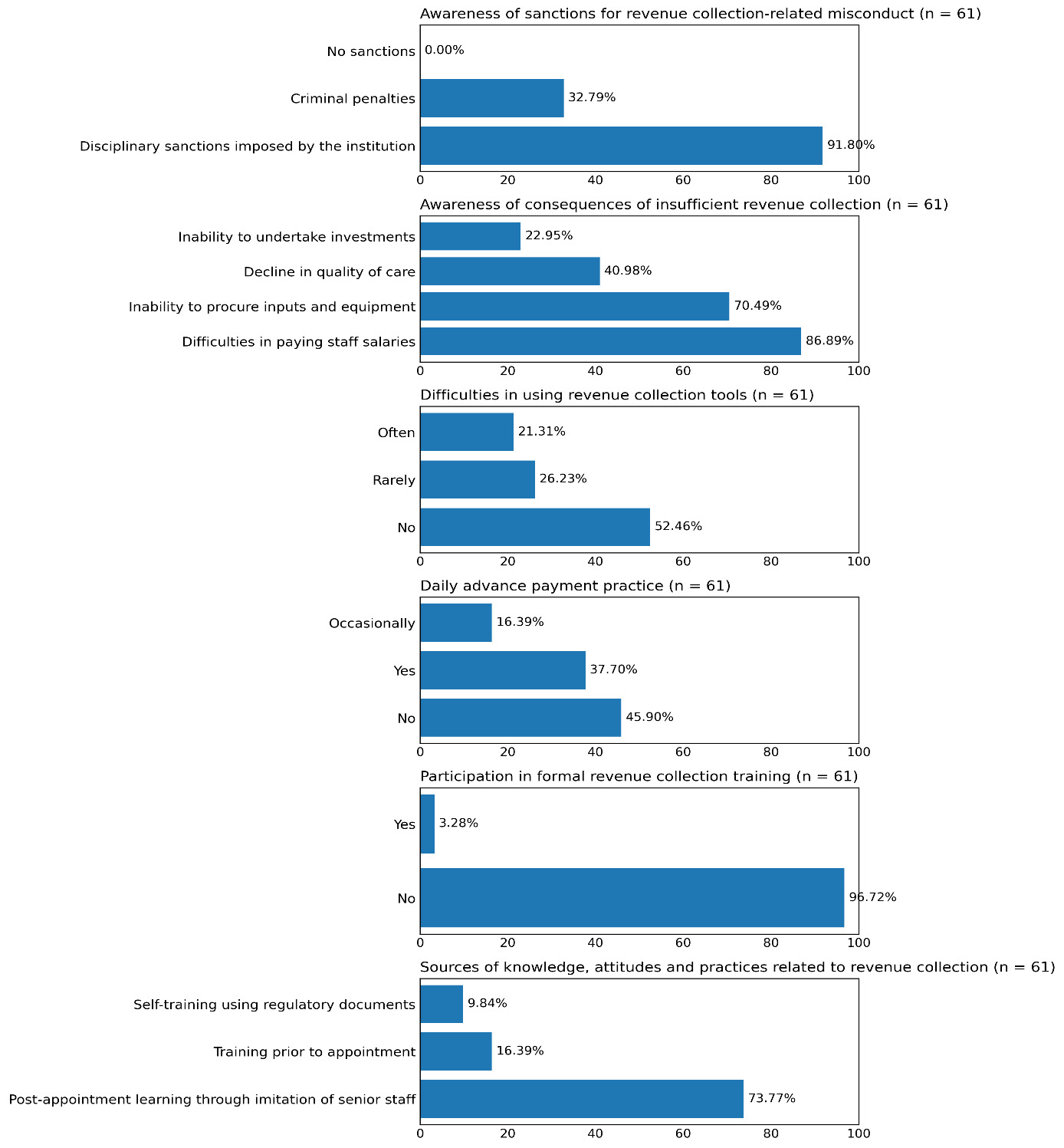

The revenue collection system relied on cashiers (n = 12), accountants (n = 7), support staff (“green-collar” workers) (n = 21) and security agents (n = 15), organised into duty and on-call teams. All key informants unanimously highlighted staffing shortages relative to workload demands.

Infrastructure and equipment

Availability of dedicated infrastructure was estimated at 17.86%. Most professionals (68.85%) considered the premises partially adequate, while 24.6% judged them to be completely inadequate.

Availability of functional IT equipment varied. An accounting software package (“Perfecto”) was in use, comprising both commercial and accounting modules. Computer availability was estimated at 61.11%, and no electronic patient record system was in place. A large majority of staff reported partial satisfaction with available equipment (77.05%) and with the availability of physical reporting tools (75.41%).

Regulatory framework

The system suffered from a lack of formalisation. No internal procedures manual was in place, and only 9.84% of staff reported having received a written job description upon appointment.

Process component of the revenue collection system

Staff characteristics and training

The staff interviewed represented a wide range of profiles (accountants, cashiers, support staff, security agents, physicians and paramedical staff), with relatively balanced representation across categories. Most respondents (77.1%) had been in their current position for less than three years, including 39.4% with one to three years of experience. The professional Bachelor’s degree was the most common qualification (30%).

Training emerged as a critical weakness: 97% (59/61) of staff had not received any formal training on revenue collection since 2021. For 73.8% of respondents, skills acquisition relied primarily on imitation of senior colleagues’ practices. In addition, 45.9% did not systematically apply the daily advance payment procedure.

Knowledge and control mechanisms

Almost all staff demonstrated good awareness of the stakes involved: 98.4% (60/61) correctly identified the negative consequences of inadequate revenue collection, including delays in salary payments, inability to procure equipment and potential deterioration in the quality of care (Figure 1). Disciplinary sanctions (91.8%) and criminal penalties (32.8%) were also cited as measures applicable in cases of misconduct. Difficulties in using available tools were frequently reported by 21.3% of respondents.

The control system included whistle-blowing mechanisms such as toll-free numbers, suggestion boxes and a communication unit. In 2023, control activities comprised 23 unannounced inspections of cash offices during the first half of the year, disciplinary sanctions against three staff members and no judicial proceedings. According to key informants, these measures contributed to improved practices among staff.

Outcome component of the revenue collection system

Financial performance

Over the period from 2021 to the first half of 2023, performance trends varied markedly across revenue categories, with substantial disparities in their respective contributions to the hospital’s overall revenue.

Overall revenue collection dynamics

The overall collection rate increased slightly from 0.80 in 2021 to 0.82 in 2022, before declining sharply to 0.62 in the first half of 2023. Internally generated revenues, which account for 61% of the hospital’s total annual revenue, recorded an average collection rate of 0.70, compared with 0.83 for external revenues (government subsidies), which were collected more regularly over the period, despite partial delays in disbursement in 2023.

Performance by revenue category

The distribution of internally generated revenues shows that laboratory services and outpatient consultations together account for nearly 80% of internal resources mobilised (Table 1).

Laboratory services constitute the main source of revenue, with an average expected revenue over three years of USD 586,852, representing 49.9% of total internal revenue. The annual collection rate for laboratory services remained consistently low and stable (approximately 0.59), below the optimal level. Outpatient consultations, the second-largest internal revenue category (29.7%), exhibited a regular and optimal collection rate, ranging from 0.79 to 0.87. Ultrasound services ranked third (11.2%) and experienced the sharpest decline in collection performance, from 1.15 in 2021 to 0.65 in 2023. Normal vaginal deliveries, the smallest internal revenue category (4.5%), recorded the highest collection rates, ranging from 0.89 to 1.16.

Financial losses

Patient absconding (94 cases) and unpaid bills (130 cases) generated substantial financial losses over the study period, amounting to USD 10,333 and USD 8,500, respectively (Table 2).

Delays in subsidy disbursement

Government subsidies were disbursed with substantial delays (Table 2). On average, the first transfer occurred 136 days after the start of the fiscal year, with a minimum delay of 90 days observed in 2021. Final transfers were recorded as late as 322 days after the beginning of the fiscal year, also in 2021.

System environment: client profile and solvency

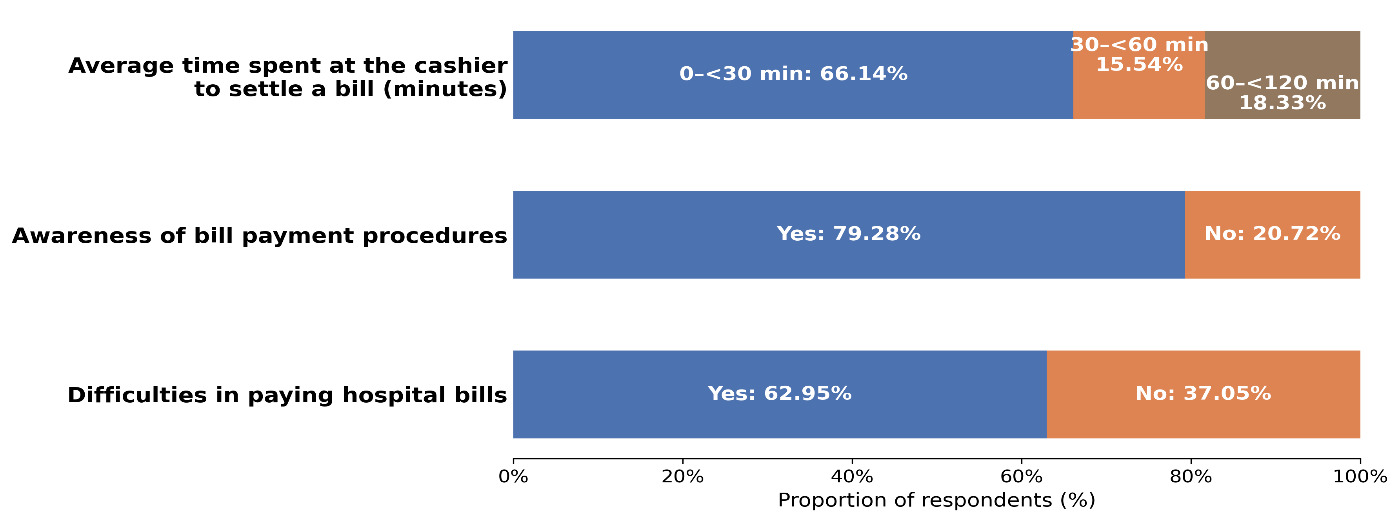

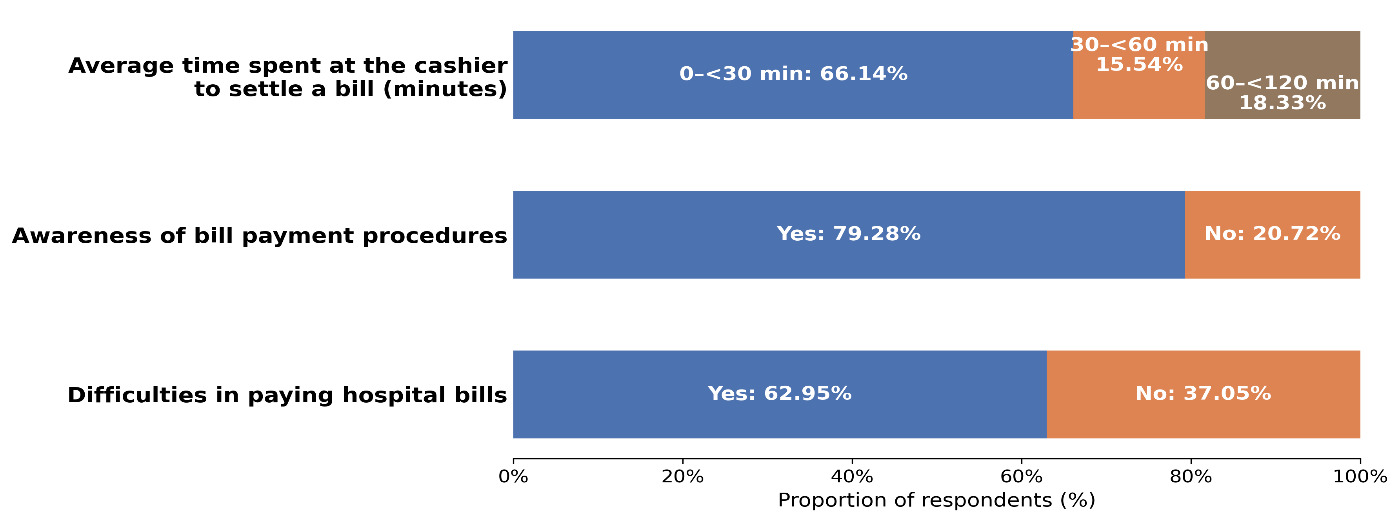

Among the 251 service users surveyed, the majority (64.1%) resided in urban areas (Figure 2). Although 79.3% of users were aware of the payment procedures, 40.2% were entirely unaware of the existence of channels for reporting malpractice.

Synthesis of factors influencing revenue collection

The analysis identified two main groups of factors affecting revenue collection performance.

Enabling factors

-

Availability of an accounting software system and systematic use of the official fee schedule.

-

Adequate level of awareness of financial stakes and sanction mechanisms among staff (62.3%).

-

Existence of functional internal control mechanisms (23 spot inspections), as well as reporting and sanction systems.

-

Positive perception of direct payment mechanisms (79%) and waiting times, considered acceptable by most users (66.1%).

-

High awareness of the consequences of insufficient revenue collection (98.4%).

-

Good knowledge of payment procedures among service users (79.3%).

Bottlenecks (constraining factors)

-

Quantitative and qualitative inadequacy of resources (human resources, infrastructure and equipment).

-

Limited formalisation of processes, including the absence of procedures manuals and written job descriptions.

-

Critical lack of staff training in revenue collection.

-

Delays and irregularity in government subsidy disbursement.

-

Significant financial losses resulting from patient absconding and unpaid bills.

DISCUSSION

This evaluation achieved its objectives by documenting the structure–process–outcome–environment components of financial resource mobilisation and by determining collection rates, including the identification of underperforming revenue categories. This systemic approach, inspired by the Donabedian framework, remains well suited to public hospitals in francophone Africa, where financial sustainability and quality of care are closely intertwined.4,8,9 It is also consistent with recent analyses of hospital governance and performance-oriented reforms in African contexts.13 Moreover, it aligns with the universal health coverage (UHC) agenda, which promotes access to care without financial hardship while highlighting the persistence of substantial inequalities in service utilisation.14

Revenue collection and economic performance

The observed annual collection rate, averaging 0.795 overall (and 0.70 for internally generated resources), remains well below the 0.90 threshold recommended for autonomous hospitals.5 This level reflects technical inefficiency in the sense of Farrell (1957),15 revealing losses in the conversion of clinical activity into effective revenue. This constitutes a clear signal of weaknesses in resource-securing mechanisms.

The pronounced heterogeneity across services, characterised by high yields for consultations and normal deliveries versus persistently low and stagnant performance for laboratory services (≈0.59), points to deficiencies in the revenue valorisation chain. This pattern is consistent with the literature on technical inefficiency in African hospital systems.16

Beyond the need for greater consideration of service-specific characteristics by the revenue collection unit, this observation also underscores organisational silos that prevent the capitalisation of experiences and successes from high-performing services, as well as the limited functionality of quality improvement mechanisms oriented towards revenue collection.

The sharp decline in ultrasound service performance (from 1.15 in 2021 to 0.65 in 2023) may be interpreted as a signal of revenue leakage, consistent with bypassing of formal payment channels, lack of traceability or non-enforcement of tariffs, as extensively documented in studies on payment failures in resource-constrained settings.17 The collection levels of 1.16 and 1.15 observed for normal deliveries and ultrasound services, respectively, although seemingly indicative of strong performance, raise concerns regarding the effectiveness of the service reporting, billing, and revenue control system. They also call into question its flexibility and its ability to adapt to special situations, such as emergencies and ad hoc service requests arising during provider–patient interactions.

From an allocative efficiency perspective, these inefficiencies, which highlight the malfunctioning of financial governance tools, limit the hospital’s ability to maximise the use of existing resources, thereby undermining its economic sustainability.18,19

Financial losses and institutional dysfunctions

Losses resulting from the weak collection of laboratory services (≈0.59), which account for nearly half of internal revenue (49.9%), combined with losses due to unpaid bills and patient absconding, represent a clear underperformance of financial governance mechanisms. Such losses are recurrent in hospital systems across sub-Saharan Africa.20 Their origins may include information asymmetry and various forms of moral hazard, often exacerbated by weak internal control systems,21 inadequate supervision mechanisms and the absence of robust formal rules.

The fact that only 9.84% of staff had a formal job description, 97% had received no training since 2021, and 73.8% relied on imitation-based learning further reinforces a high-risk operational environment. These characteristics of the workforce and its operating environment indicate that the observed gaps are structural rather than cyclical, thereby calling for more decisive and sustained measures targeting both of these pillars.

These losses constitute a major opportunity cost, leading to:

-

reduced working capital;

-

procurement delays;

-

deterioration in quality of care;

-

increased marginal costs.

They contribute to a vicious cycle well described in the literature: inefficiency → losses → reduced investment → quality deterioration → declining utilisation.20

System vulnerability and economic governance failures

Public resources, although critical, are characterised by extreme volatility, with disbursement delays reaching up to 322 days. This unpredictability, also observed in other African settings,22 undermines planning, investment and economic performance. It runs counter to the hospital-as-an-enterprise paradigm, which requires a stable financial base to sustain quality, innovation and investment.13

Although 23 unannounced inspections were conducted in 2023, in line with national directives and findings from other studies in Benin,11 these efforts remain insufficient in the absence of formal procedures, a structured information system and full digitalisation of revenue collection.

The lack of integration of Revenue Cycle Management substantially limits traceability and financial stability.23

Socio-economic context and financial risks for households

Payment difficulties reported by service users reflect the predominance of out-of-pocket financing, a phenomenon widely documented in Africa.14,24 This context increases unpaid bills, weakens cash flow and fuels an adverse cycle: limited solvency → non-payment → declining quality → reduced utilisation.25 Expansion of insurance mechanisms, supported by robust information systems, is among the most well-documented levers for reducing catastrophic health expenditures.14

Overall synthesis

The integrated analysis highlights a financial mobilisation system that is:

-

marked by persistent technical inefficiency16;

-

characterised by avoidable financial losses;

-

dependent on irregular subsidies;

-

affected by deficits in formalisation;

-

weakened by limited household solvency.

These constraints, also reported in other low- and middle-income countries,13 hinder progress towards UHC. Strengthening financial governance, fully digitalising revenue collection, diversifying funding sources and expanding insurance mechanisms emerge as strategic priorities.

Study limitations

This study provides an in-depth systemic analysis of hospital financial mobilisation. However, its cross-sectional design limits causal inference. Variable quality of administrative data may have affected some estimates. Stakeholder perceptions may be subject to reporting bias despite triangulation. Finally, conducting the study in a single hospital limits external validity. Multi-site and longitudinal studies would enhance the robustness of these findings.

CONCLUSIONS

This study reveals a fragile revenue collection model affected by technical, organisational and economic inefficiencies. Despite a renewed institutional framework, the hospital struggles to convert clinical activity into effective revenue. Financial losses, dependence on irregular subsidies and limited household solvency exacerbate the hospital’s economic vulnerability.

In the short term, strengthening hospital governance, through improved capacity building of revenue collection staff, rigorous implementation of updated and more appropriate procedures, digitalisation of the revenue collection system, the development of tailored revenue collection strategies (particularly for laboratory services), and increased accountability of providers, would help address existing gaps. This strategy, together with the medium- and long-term expansion of financial protection to all households through health insurance, constitutes a set of fundamental levers for improving hospital performance and advancing progress towards universal health coverage.

Acknowledgements

The authors are grateful to IRSP, the Ministry of Health, and the staff of the Centre Hospitalier Universitaire de la Mère et de l’Enfant–Lagune (CHUMEL) for their valuable support and collaboration.

Disclaimer

The views expressed in this article are those of the authors and do not necessarily represent the official position of their institutions.

Ethics statement

This study was approved by the Ethics Committee board of the Regional Institute of Public Health (IRSP). Informed consent was obtained from all participants prior to data collection. Confidentiality and anonymity were strictly maintained throughout the study

Data availability

The datasets generated and analysed during the current study are available from the corresponding author upon reasonable request.

Funding

The research presented in this manuscript received no external funding.

Authorship contributions

All authors meet the ICMJE authorship criteria, contributed significantly to the work, and approved the final version of the manuscript.

Disclosure of interest

The authors declare that they have no competing interests

Correspondence to:

Name Surname: Lamidhi SALAMI

Institution: Regional Institute of Public Health

Address: Ouidah

Country: Benin

email@email: s.lamidhi@yahoo.com