Catastrophic expenditures are direct health-related expenses incurred by a household that exceed a certain proportion of the household’s financial means of the latter1,2 i.e. 10%3 or 25% of total household income.4–6 Such situation is likely to reduce household consumption for other basic needs.7 Catastrophic expenditure is also defined as reaching the threshold of 40% of the household’s disposable income after basic needs have been substracted.8–11

Direct payments are the main way of payment for healthcare in emerging countries.12 In 2015. the year of the adoption of the Sustainable Development Goals (SDGs). nearly one billion people worldwide incurred catastrophic health expenditures at the threshold of 10% of total household income. and around 200 million people incurred direct health expenditures exceeding 25% of the household budget.7,13,14

In Sub-Saharan Africa. within 2000 and 2021. nearly half a million households incurred catastrophic expenditure at a threshold of 10% of total household expenditure. representing an incidence of 16.5%. and about 800 000 households incurred catastrophic expenditure at a threshold of 40% of non-food household expenditure. representing an incidence of 8.7%.12

Households located in rural areas. with lower socio-economic status. with members suffering from chronic illnesses. with children. with elderly members. or with large households are at greater risk of experiencing catastrophic healthcare expenditure. It has also been revealed that out-of-pocket expenses increase the incidence of catastrophic healthcare expenses and push households into poverty.15

In the Democratic Republic of Congo. a study carried out in Kinshasa estimated the incidence of catastrophic health expenditure at the 10% threshold at 46.4%. and another in the city of Lubumbashi at 16.0% at the 40% threshold of disposable household income after subsistence needs have been met.5,6

The factors associated with catastrophic expenditure are: socio-demographic (location. household size) and economic ( health insurance coverage. economic well-being and occupation of household’s head): rural residence is more likely to lead to catastrophic expenditure than urban residence16,17 and household size18–21 influence catastrophic spending. Some authors also mention the occupation of the head of Household. particularly the disemployment.22,23 Lack of health insurance coverage [20,26.27] as well as the poverty aspect of economic well-being24–27 are also associated to catastrophic health expenditure. Households with a large number of members [ 24, 31.] those living in rural areas.28 and those whose head is unemployed are more likely to fall prey to catastrophic healthcare expenditure. Catastrophic spending has an impact on impoverishment and the use of healthcare services.29 Indeed. to access healthcare. some households sell their assets and/or incur debts. thus maintaining a cycle of poverty.30–32 Access to healthcare is limited for those who are simply unable to pay for it directly [33. 36].

Households in lower socio-economic groups tend to resort to borrowing. and often find themselves unable to repay their debts. thus accentuating catastrophic healthcare expenditure.33

Out-of-pocket healthcare expenses expose households to the risk of financial catastrophe and poverty when they result in significant dissavings or the sale of key household assets. Without sufficient liquidity. households are thus forced to resort to various methods to finance healthcare further impoverishing the poorest households.33 such as selling assets. borrowing. reducing food consumption. taking children out of school and even giving up or delaying seeking medical care (39–41)"]. And even when small. these financial health costs are disastrous for poor households34 further exposing them to the risk of catastrophic health expenses.35,36 Wealthy households are not spared from this risk either. when health expenses are high.37

Catastrophic health expenditures. and consequences of out-of-pocket payments. are obstacle in the progress toward universal health coverage38

Improving financial protection to mitigate the impact of catastrophic spending on households has received considerable attention.12 Indeed. the DRC member of the United Nations included in 2015 the incidence of catastrophic health expenditure as a key indicator to monitor progress towards Universal Health Coverage (UHC) (SDG 3.8.2).30,39 Reducing the incidence of catastrophic health expenditure is one of the key objectives of global. regional and national health policy in support of UHC and human development.30,32,39,40 In the era of universal health coverage, every effort is being made to guarantee financial accessibility to healthcare on the one hand, and to reduce catastrophic out-of-pocket expenditure as much as possible on the other.

Our study aims to determine the prevalence of households that fall into catastrophic expenditure and socio-economic profile of households facing catastrophic health expenditures in the Democratic Republic of Congo (DRC). Currently, there is limited information available on this subject in the specific context of the DRC, and the studies conducted are constrained. Therefore, the findings of our study are crucial as they will help bridge this gap in the scientific literature and provide relevant data to justify the imperative transition towards universal health coverage.

In the Democratic Republic of Congo (DRC), direct payments are the predominant mode of healthcare financing, accounting for over 70% of total healthcare expenditures. Mechanisms for risk pooling and resource sharing are nearly absent, with households and external donors respectively bearing around 43% and 40% of the financial burden of healthcare, while the government’s contribution remains minimal, at around 15%.41 In this context, households are highly vulnerable to catastrophic health expenditures when seeking care.

Against the backdrop of the country’s commitment to achieving Universal Health Coverage (UHC), our study aims to assess the magnitude of catastrophic health expenditures and identify the associated factors among households in the Kongo Central province, where a significant portion of the population resides in rural areas. By exploring this specific context, our research aims to provide essential insights into the socio-economic determinants of catastrophic health expenditures, thereby contributing to policy decisions aimed at strengthening healthcare financing systems and expanding access to affordable and equitable healthcare services. Ultimately, this study is part of an effort to improve access to quality healthcare for the entire Congolese population and reduce health inequalities. And this lead to three research questions:

-

What is the magnitude of catastrophic expenditures related to the utilization of healthcare services by households in the Health Zones of Kongo Central?

-

What are the socio-demographic and socio-economic characteristics of households in the studied geographical areas?

-

What are the associated factors or determinants that contribute to households experiencing catastrophic expenditure when utilizing healthcare services?

METHODS

This study constitutes a secondary analysis of data derived from a survey aimed at assessing the implementation and functioning of Community Action Cells (CACs) and Health Area Development Committees (HADC) across seven health zones within the Kongo Provincial Health Division. Ethical clearance for the primary study was obtained from the Ethics Committee of Kinshasa Study of Public Health. and informed consent was obtained from all participants.

Respondents were mothers or caregivers. The target population was households with a child aged 0-59 months at the time of the survey and residing at the survey site for at least 6 months. For this analysis. the statistical unit was a household with a child under 5 years old and a household that have incurred health expense in favor of the child during the last two weeks.

Setting

The survey took place in Kongo-Central province between September 12 and November 12, 2022. It covered the Muanda, Boma, and Matadi Health Zones.

The Province of Kongo-Central is subdivided into urban and rural entities. The urban entities comprise 2 towns (Matadi and Boma). 6 Communes (3 for Matadi and 3 for Boma) and 34 health districts. The rural entities are grouped into 10 Territories (Lukula. Tshela. Seke-Banza. Mbanza-Ngungu. Luozi. Songololo. Kasangulu. Madimba. Kimvula and Muanda). These territories are subdivided into 55 Sectors and 6.514 Villages. The population of Kongo Central is estimated at 4.246.503 in 2020. with a density of 79 inhabitants/km2. and 1.061.1322 households with an average size of 5.3.42 In 2019. life expectancy was 67.7 years and the number of children under the age of five was 1.289.000. whose 643.000 boys and 646.000 girls.43 Agriculture is the main occupation of the population. especially in rural areas. and is mainly subsistence farming. Small livestock and poultry farming are practiced in rural areas. while large livestock farming is practiced in Cataractes and Boma. Artisanal fishing is practiced along the Congo River and the Atlantic Ocean. The main agricultural crops are maize. groundnuts. cassava. plantains. beans. palm oil and vegetables in the Mbanza Ngungu territory. In urban areas. public administration and a few businesses keep the population busy. but informal activity (petty trade and the like) is flourishing. Formal economic activity is supported by the commercial company for transport. post and telecommunications (SCTP). with its two international ports of Boma and Matadi. followed by the private port of Matadi Getway Terminal (MGT). and by industrial companies (Lukala cement plant . National cement plant. NYUMBA KIBA. the Kwilu ngongo sugar mill. etc.). which constitute the economic lungs of the province. Mining is not highly developed. although the subsoil is rich in minerals such as bituminous shale. manganese. marble. gold and diamonds. Oil is exploited in the Muanda Health Zone.42 Average household size is a determining factor in household living conditions. The smaller the household size. the less exposed it is to poverty. and vice versa.44

Sample size and sampling technique

The primary data contained 2520 households. according to a reasoned choice. our study included three of the seven health zones. then 1242 households. We have taken into account households having carried out healthcare expense. We retained a sample size of 205 households. In the primary study. seven health zones were selected: these were the intervention zones targeted by the non-governmental organization Primary Health Care in Rural Areas (SANRU) for the implementation (revitalization) of community participation bodies (CAC and HADC).

Clustered Lot Quality Assurance Sampling (LQAS) was used through a 3-stage sampling process. in each health zone:

-

In the first stage. six health areas were randomly selected in each of the health zones to serve as a cluster.

-

In the second stage. six villages/locations/avenues were selected in each cluster (AS) for a total of 504 villages/locations/avenues for the whole study.

-

In the third stage. 10 households with at least one child aged 0-59 months were randomly selected and surveyed in each village/locality/venue. for a total at least of 400 households per health area.

According to a reasoned choice. our secondary analysis focused on three of these ZS. two urban and one rural. in order to compare the proportions of households with catastrophic expenditure in these different zones.

Data collection, Variables and data processing and analysis*

Data collection

The data come from a mixed-method. cross-sectional analytic household survey conducted by the Kinshasa School of Health on a sample of 2.520 households in seven health zones in 2022. The aim of the study was to assess the organization. functioning and involvement of the community system in promotional. preventive and curative activities in the targeted ZS in the provinces of Kinshasa and Kongo-Central. Their study population was mothers and caregivers.

After obtaining permission to use the data from the Kinshasa School of Public Health. we extracted data on socio-demographic (household residence and household size) and socio-economic aspects (occupation of household head. health insurance coverage. economic well-being). Our study was carried out in March and April 2023 and used only quantitative data from the primary study

Variables

Dependent variable: Catastrophic health expenditure: Obtained by taking the quotient of health expenditure by the total monthly income household. Catastrophic health expenditure was presented at thresholds of 10% and 25% of total household income.

Independent variables: location. household size. household head occupation. health insurance coverage. and economic well-being.

Economic well-being: was assessed by principal component analysis (PCA). it results on 5 categories that we dichotomized in two: poor (poorest and poor) and rich (middle income. rich. richest).

Data processing and analysis

After data extraction. quantitative data from the Muanda. Boma and Matadi HZs were analyzed. Data were entered into SPSS version 26 and analyzed using the same software. Descriptive analyses included frequencies and percentages. Bivariate analyses were performed to see the association between catastrophic health expenditure at 10% or 25% and the independent variables (location. household size. household head occupation. health insurance coverage. and economic well-being). Multiple logistic regressions were performed respectively at the 10% and 25% thresholds of income to control for confounding. The association was statistically significant if the p-value was strictly less than 0.05.

RESULTS

The Socio-demographic and economic characteristics of the sample

The socio-demographic characteristics of respondents show that more than four fifths were women (96.1%). around half completed primary education (53.3%). Nearly half the respondents were living common-law (46.3%). the majority of respondents were members of the revivalist church (57.1). According to their employment. the modal category were housewives with more than one quarter (27.1%). and the majority of households were in rural areas (61.0%).

Concerning the socio-economic characteristics of households. the majority of household heads were administrative. employed or retired (26.8%). the vast majority of households had more than 6 members (94.1%). more than half of households were not covered by health insurance (88.3%.) And more than half were wealthy (60%). Having considered the resourceful as unemployed. the majority of household heads were employees (77.1%).

The magnitude of catastrophic health expenditure for the care of children under Five years-old

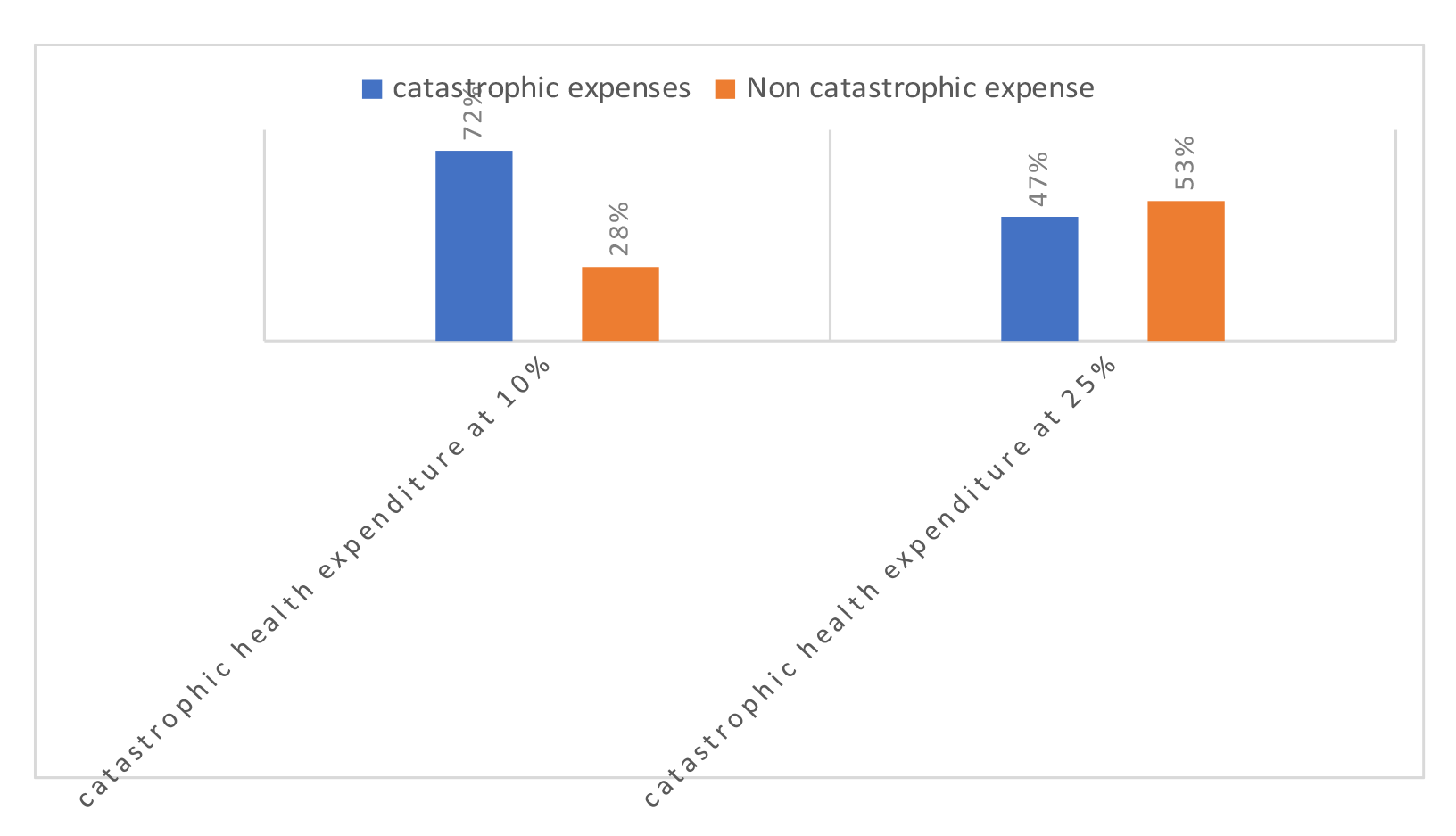

Almost three-quarters of households (72%) have incurred catastrophic health expenses at the 10% threshold and under half of all households (47%) have incurred catastrophic healthcare costs at the 25% threshold (Figure 1).

The proportion of catastrophic expenditure at the 10% threshold is significantly higher from that obtained at the 25% threshold (p <0.0001).

More than half of urban households have incurred catastrophic healthcare costs at the 10 and 25% thresholds. More than half of households between one and six in size fell into catastrophic health expenditure. The majority of households with no health coverage incurred health expenses at the 10 and 25% thresholds. Just under half of poor households incurred catastrophic health expenses at the 10 and 25% thresholds. The majority of households with an unemployed head fell into catastrophic health expenditure at the 10% and 25% thresholds. (Table 1)

The table 1 also shows that no variable is significantly associated with catastrophic expenditure at the 10% threshold however at 25 % the table shows that two variables are significantly associated with catastrophic expenditure at the 25% level: economic well-being and employment. Households with poor heads are 1.8 times more exposed to catastrophic expenditure than those with rich heads. And households whose heads are unemployed are 1.9 times more exposed than those whose heads are employed.

After adjusting for all independent variables. only being poor remained significantly associated with the dependent variable: catastrophic health expenditure at the 25% threshold. Poor households are 1.8 times more exposed to catastrophic expenditure than rich households (Table 2).

DISCUSSION

A total of 205 households were interviewed in three health zones. The vast majority were women (96.1%); more than half had completed primary education (53.3%). Nearly half the respondents (46.3%) were living common-law, and the majority (57.1 %) were members of the revivalist church, which could be explained by the fact that these churches are expanding rapidly throughout the country. The majority of respondents were housewives (27.1%), and the majority of households were made up of more than 6 members (94.1%). These results are slightly similar to those obtained in a study carried out in Nigeria in 2018, where 77.5% of households were made up of more than 5 members,12 which increases the risk of catastrophic expenditure.18

Almost all households (88.3%) were not covered by insurance and therefore made out of pocket payments for healthcare. These results are close to those reported by a study carried out in Goma, DRC in 2021, where 89.9% of households were uninsured.41

The majority of households were not covered by insurance and therefore made out-of-pocket payments for health care. These results are close to those reported by the National Strategic Plan for Universal Health Coverage. As well as by a study carried out in Goma in the DRC in 2021 and further confirmed by the PNDS, of which 89.9% of households were not insured.30,43

Regarding the magnitude of catastrophic expenditure, at the 10% threshold, the majority of our households (71.7%) made catastrophic expenditure, which is far higher than the result found in a study conducted in Kinshasa, in 2015 when they reached 46.4%.45 As for the 25% threshold, around one in two households (47%) made catastrophic expenditures, figures similar to a study conducted in Goma in 2021.43 Only children under the age of five were included in the health expenditure. This would imply that the prevalence could be even higher if we took into account the healthcare expenses of all family members.

In terms of socio-demographic and socio-economic profile, the majority of households with catastrophic expenditure at the 10 and 25% thresholds were urban. Contrary results were found in a study carried out in 2022 in Sudan, with 74.3% of households in rural areas at the 10% threshold and 79.5% in urban areas.18 More than half of households with a size between 1 and 6 fell into catastrophic health expenditure at both thresholds, corroborating the findings of Elhaj et al, who stipulate that as the number of household members’ increases, catastrophic health expenditure decreases,18 Kimani et al found different results, showing that an increase in household size increases the probability of incurring catastrophic healthcare costs. A larger household size means a greater likelihood of a person becoming ill. What’s more, if the disease is contagious, it’s more likely that more people will be ill in a larger household. Consequently, we would expect healthcare spending to be higher in larger households. Since higher healthcare expenditure is more likely to result in catastrophic healthcare expenditure, household size should also increase the likelihood of catastrophic healthcare expenditure.

The majority of households with catastrophic expenditure at both thresholds were not covered by health insurance, as the vast majority of the DRC population has no form of social security,46 those who are not covered are more likely to incur catastrophic expenses.37 The majority of wealthy households made catastrophic expenditures at the different thresholds, the same results were found in a study conducted in 2016 in Kenya where the majority of wealthy households fell into catastrophic expenditures37 this can also be explained by the fact that the richer a household is, the more it seeks quality care, which is more expensive.18 According to Elhaj et al, the appreciation of the household head’s affluence encourages households to spend more on healthcare. The vast majority of employees incurred catastrophic health expenses.18 At the 10% threshold, no independent variable was associated with catastrophic healthcare expenditure. Poverty was significantly associated with catastrophic expenditure at 25% (OR: 1.866(1.060-3.284)), as was the fact that the head of household was unemployed (OR: 1.950(1.006-3.782)). After adjustment for variables, only being poor was associated with catastrophic health expenditure (OR: 1.833(1.036-3.243)), similar results were found in a study conducted in Uganda in 2020 where the poorest households experienced a higher incidence of catastrophic payments.24 This demonstrates that direct health spending is regressive and that there is a lack of protection for the poor against such high expenditure. The magnitude of catastrophic health expenditure at the 10% threshold was 72%, and 47% at the 25% threshold, a significant difference. The same was true for health insurance coverage at the 10% and 25% thresholds.

Unemployed was found to no longer be associated after adjustment; however, due to its wide confidence interval, further study with a larger sample size is needed to increase precision.

This study has certain limitations: The health expenses incurred relate to a two-week period preceding the interview. The measurement of income was soft. To increase the accuracy, the study takes into account all sources reporting an entry into the household, not just the declared salary.

CONCLUSIONS

Our study took place in the health zones of Muanda, Boma and Matadi in the Provincial Health Division of Kongo-Central. Its main objective was to describe the socio-demographic and economic profile of households with catastrophic expenditures in these HZs in October 2022. The prevalence of catastrophic health expenditure found in Kongo Central’s port area is significantly higher compared to that of Sub-Saharan Africa. Poor household was more associated with catastrophic expenditure at 25%. The majority of the population is thus exposed to falling further into poverty; underscoring the necessity for the country to establish a healthcare coverage system.

These results can be generalized to the population residing in the port area of Kongo Central.

Acknowledgements

We are grateful to Mungala Mutombo Pomie, Lutandila Diazola Papy, and Aurore Beia.

Ethics statement

ESP/CE/118/2022 of September 12, 2022, Kinshasa School of Public Health Ethics committee. The informed consent was obtained from all participants involved in the study

Funding

The research presented in the manuscript received a funding of Santé Rurale,SANRU-SARL, Global Fund (NMF3).

Authorship contributions

All the authors mentioned have fulfilled those 4 criteria:

-Substantial contributions to the conception or design of the work; or the acquisition, analysis, or interpretation of data for the work; AND

-

Drafting the work or reviewing it critically for important intellectual content; AND

-

Final approval of the version to be published; AND

-

Agreement to be accountable for all aspects of the work in ensuring that questions related to the accuracy or integrity of any part of the work are appropriately investigated and resolved.

Disclosure of interest

The authors completed the ICMJE Disclosure of Interest Form and disclose no conflicts of interests.

Correspondence to:

Masokolo Malamba Bijou Laetitia

Department of Nutrition, Kinshasa School of Public Health

Kinshasa, Lemba

The Democratic Republic of Congo

bijou.masokolo@unikin.ac.cd